What is the In banking, " ACH " stands for " Automated Clearing House", which is a system that coordinates automated payments and money transfers. ACH allows money to be transferred between financial institutions using electronic payments and automated transfers.

The Key Takeaways

- The automated clearinghouse (ACH) network is used to process electronic payments, without the use of wire transfers, cash, or credit cards.

- ACH transfers automate payments such as employee wages or bills.

- ACH transfers are sometimes referred as electronic funds transfers (EFT).

How ACH Works

The ACH system is a group of computers that work together to automatically process payments. You don’t have to handle payments manually (either on your part or that of the biller). ACH is a batch processing system which processes millions of payments each day.

This network relies on two “clearinghouses” to process all requests. The network allows for efficient matching between financial institutions.

Depending on the context, ACH transfers could mean a number of things.

ACH Transfers in Bank Statements

ACH is a term that you may see on your statements or transaction history. It means an electronic payment was made using your checking account details. Below are some examples of ACH transactions. You must provide your account number and routing numbers to authorize an ACH transaction to transfer funds into or out of your account.

You can now transfer money using ACH on your bills

When you view a bill with ACH, it means that you can pay bills electronically. Other terms are eChecks or EFT. You can pay from your account directly instead of writing checks or entering credit card numbers every time. In some cases thecontrols when payment is made (the funds are only moved when you request payment). You may also be required to have money in your account at the time of your bill’s due date.

Note:

Even though automatic payments are made, it is important to keep an eye on the accounts you have and how they are being used.

What does ACH do for consumers?

You may be able to enjoy a number of benefits if you are an individual .

- You will receive your payment quickly, securely, and reliably. Avoid the hassle of having to wait for your pay check or depositing it at the bank.

- Automate payments so that you don’t forget to pay and your payments are always on time.

- Online purchases can be made without a credit card or check. You can pay instantly and avoid credit-card processing fees.

- Reduce the amount of paperwork that contains your account information. It will reduce the likelihood of fraud on your account.

It is important to note that ACH gives businesses direct access to the checking account of consumers. The money is taken to pay bills, whether you are ready to pay them or not. You may prefer to pay in a different manner if you are short of funds. If you’re short on funds, you may want to pay only the most important bills first.

For more information on how to use ACH as a consumer, please read Setting up ACH Debit.

What is ACH for Business?

You can benefit from the following if you own a business :

- Transferring money is a low-cost and non-labor intensive way.

- Paying employees electronically without printing checks or paying postage

- No more cash! Receive payments from customers quickly, easily and regularly.

- Payment processing fees are lower than swipe fees

- Paying vendors or receiving payments from suppliers in a safe, easy-to-track way (every transaction is recorded instantly electronically)

Businesses have the same problems as consumers. There is a direct connection to your checking account and any mistakes or unexpected withdrawals could cause issues. Businesses can also be faced with customers who reverse charges or take back payments. It’s more difficult to reverse an ACH Payment, than it is to do so with a credit card. 4

Note:

Businesses must be extra vigilant in monitoring for fraud. Business accounts are not protected to the same extent as consumer accounts. You may have to take responsibility for recovering funds that leave your account.

Businesses may also need to invest in software or time and resources to transition to ACH transfers. They’ll likely recover these costs over time.

Read about ACH Processing to learn more about how businesses use ACH.

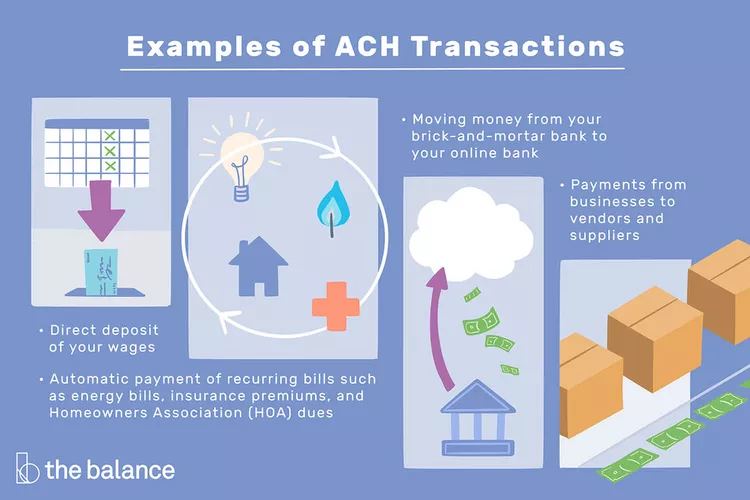

Examples of ACH Transactions

You may have used ACH more than you think. Everyday transactions that businesses and individuals make include:

- Direct deposit of your wage (from your employer into your bank account).

- Automated payment of recurring charges such as energy bills and insurance premiums . You can set up ACH by submitting a voided cheque to your biller.

- Payments by businesses to suppliers and vendors

- Money transfer from your brick and mortar bank to your online account

Wire transfers vs. ACH

| ACH | WIRE TRANSFERS |

|---|---|

| Free is a good term to describe the service. | It usually comes with a charge |

| Domestic and International | Domestic and International |

Wire transfer is another electronic payment method. There are differences between ACH and wire transfers, despite some similarities. Until recently, ACH transactions were not allowed to be done internationally.

Note:

A ACH transfer is also known as an electronic funds transfer. A wire transfer is not an EFT.

The pros and cons of ACH transactions

Pros

- Pay faster

- Convenient

You can also find out more about Cons

- Direct access

- Overdraft fees

Pros Explained

- Get Paid Faster You can receive payments faster using ACH. You don’t need to wait for the check to clear.

- Convenient : You can automate payments for bills to avoid late fees or missed payments. Make online purchases using a credit card without the need to use a check. Minimize paper records containing sensitive banking information.

Cons explained

- Direct Access: Companies can access your account directly. Be careful with whom you share your bank information.

- Overdraft Fees: Automatic payments are made whether or not funds are in your account. This can result in overdraft charges.

Types of ACH transfers

ACH transactions are not currently done in real time. Banks use batch processing to process all of the requests for a day at once. You won’t be paid right away after your employer has authorized payment. The transaction will take one to two business days for it to be processed. There are plans for ACH payments to be accelerated, and certain transactions have already started receiving same-day payments.

ACH transactions can take two forms.

- Direct Deposit is a payment made to a recipient, like a paycheck from your employer or Social Security payments paid into your account.

- Direct Paymentsare requests for funds to be withdrawn from an account. Direct payments are made when utility bills are automatically deducted from your checking account.

FAQs (Frequently Asked Questions)

What is the difference between ACH (automatic clearing house) and direct deposit?

A direct ACH deposit can be described as a particular type of ACH transaction. Direct deposits are any deposits made directly to your bank account by an employer, such as wages. ACH transactions includes direct deposits and payments to others. 10

What are the requirements for ACH payments?

You’ll need both the recipient’s account and routing numbers to process an ACH.

Banks charge for ACH payments

Banks don’t charge for ACH transactions. ACH transactions can trigger Overdraft Fees if there are insufficient funds to cover the payment.